The Standard Group Plc is a multi-media organization with investments in media

platforms spanning newspaper print operations, television, radio broadcasting,

digital and online services. The Standard Group is recognized as a leading

multi-media house in Kenya with a key influence in matters of national and

international interest.

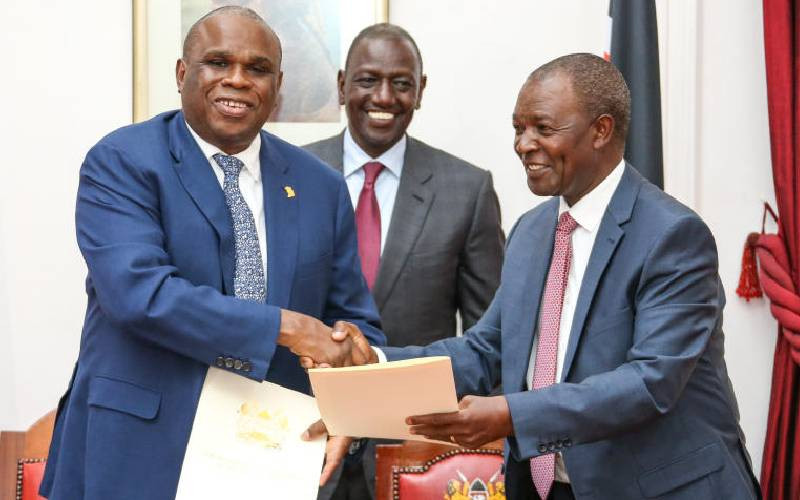

AfriExim Bank President Benedict Oramah and Treasury Cabinet Secretary Njuguna Ndung'u signed a Sh400 billion loan deal in the presence of President William Ruto at State House, Nairobi. [PCS]

The cash-strapped government has received a huge financial boost after inking a $3 billion (Sh407 billion) loan deal that will cushion the battered economy against external shocks.

The three-year loan financing programme from the African Export-Import Bank (Afreximbank) was signed yesterday at State House, Nairobi.

The deal that allows Kenya to draw down part of the funds immediately is expected to give Kenya 'breathing space' amid a raging economic crisis that threatens to snowball into a deeper crisis unless arrested early.

Afreximbank, which counts 50 African countries among its shareholders, finances and promotes intra- and extra-African trade.

Its president, Benedict Oramah, said the loan will help Kenya overcome the "transitory shocks" it is facing amid the Russia-Ukraine crisis, which has caused energy and food disruptions and tightened global credit conditions.

"The key goals are to have Kenya manage the transitory shocks that Kenya, African, and indeed the global economies are going through today," said Prof Oramah at a press conference in Nairobi yesterday.

"We have the energy problems caused by the conflict in Ukraine, also the problem with the challenge of fertiliser, and also the debt crisis and the rising interest rates."

The programme will support viable trade and trade-related project ventures in both the private and public sectors.

The financing package will be implemented using several instruments including loans, guarantee facilities, investment banking and advisory services.

The Afreximbank loan comes as a relief as it is expected to offer the Ruto government breathing space amid an escalating debt burden.

Ballooning inflation, escalating borrowing costs and a strong dollar have made repaying sovereign loans and raising money significantly more expensive for Kenya amid fears of default.

The cash shortage has seen the government struggle to pay civil servants and disburse county government obligations.

The shilling has weakened against the dollar, piling further pressure on Kenyans enduring high cost of living crisis that has plunged many into poverty and fuelled political unrest.

"This programme is a step forward in our economic recovery agenda and will assist the government following shocks occasioned by the Covid-19 pandemic as well as the global economic crisis," said President William Ruto after the loan signing.

"On agriculture, the facility will be beneficial in bringing down the cost of fertiliser and other essential commodities that are very critical as a way of further bringing down the cost of living in the country."

Opposition-allied protesters yesterday took to the streets in several areas of the country to voice anger at the dire economic situation and political deadlock.

Prevailing debt crisis

The Ruto administration is now banking on regional lenders such as Afreximbank and global lenders including the International Monetary Fund (IMF) and the World Bank for help to stem the economic crisis.

Cairo-based Afreximbank, which was founded in 1993 under the auspices of the African Development Bank, is also seeking to set up a branch in Nairobi.

Treasury Cabinet Secretary Njuguna Ndung'u said the credit programme will help Kenya manage the prevailing debt crisis but also accelerate economic recovery.

AfreximBank, which manages assets in excess of $22 billion (Sh2.9 trillion) will under the loan deal help Kenya spur trade by facilitating Kenyan traders to export their goods in the region and building industrial parks in the country, said Trade Cabinet Secretary Moses Kuria.

The government is also angling for new financing from the IMF and the World Bank, which are expected to give $1.25 billion (Sh169.8 billion) budgetary support in the coming weeks.

IMF teams are expected in the country this week ahead of the possible engagement.

Central Bank of Kenya (CBK) Governor Patrick Njoroge said recently the government is in talks for new funding from IMF to support falling foreign exchange reserves.

He said Kenya is also seeking a new loan under the IMF's Resilience and Sustainability Trust to help countries ensure sustainable growth.

The loans come amid narrowing borrowing options that have locked the National Treasury out of both domestic and global capital markets.

The disbursements could help Treasury avert a looming debt crisis, analysts say.

Kenya Kwanza policymakers are struggling with the dual challenge of managing overseas debt repayments while meeting domestic needs.

The double burden of rising prices and high debt has put pressure on the Ruto administration at a time Kenyans are bearing the brunt of the economic crisis.

The Standard Group Plc is a multi-media organization with investments in media

platforms spanning newspaper print operations, television, radio broadcasting,

digital and online services. The Standard Group is recognized as a leading

multi-media house in Kenya with a key influence in matters of national and

international interest.

The Standard Group Plc is a multi-media organization with investments in media

platforms spanning newspaper print operations, television, radio broadcasting,

digital and online services. The Standard Group is recognized as a leading

multi-media house in Kenya with a key influence in matters of national and

international interest.