×

The Standard e-Paper

Fearless, Trusted News

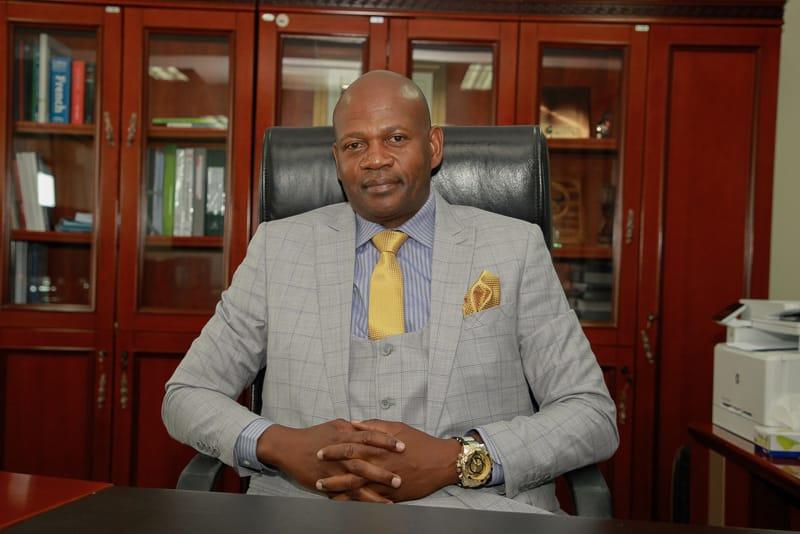

Stung by non-performing loans, Shelter Afrique has changed tack to focus on large scale projects and partnerships. The Pan-African lender’s Managing Director Andrew Chimphondah talks to Home & Away on their new direction.

You have been very vocal about affordable housing, is this an area Shelter Afrique will be going into more?

Subscribe to our newsletter and stay updated on the latest developments and special offers!