×

The Standard e-Paper

Stay Informed, Even Offline

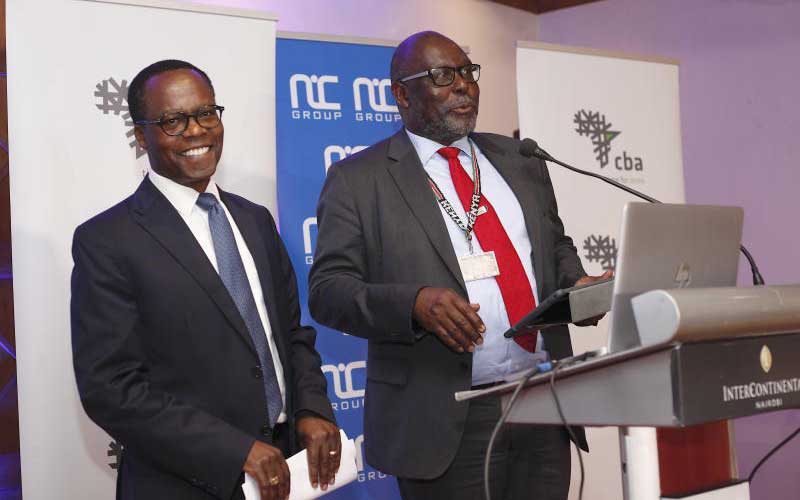

When Kenya’s two powerful bankers - Commercial Bank of Africa (CBA) Group Managing Director Isaac Awuondo and NIC Bank boss John Gachora - recently shared the stage as a show of equal footing in the merger of NIC Bank and CBA, questions were raised as to who will be left standing at the end of the year.

Head of banking research at Ecobank Capital, George Bodo voiced this question in the stormy waters of the merger as to how the management change.

Subscribe to our newsletter and stay updated on the latest developments and special offers!