×

The Standard e-Paper

Join Thousands of Readers

Audio By Vocalize

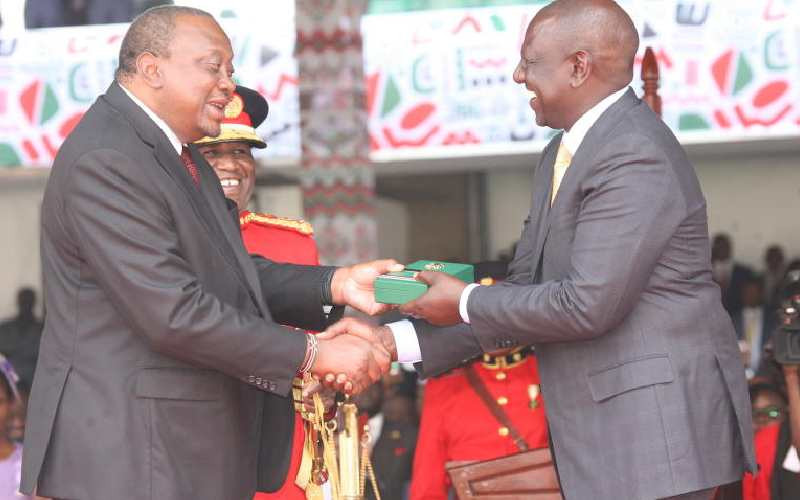

President William Ruto and Uhuru Kenyatta at Kasarani stadium on September 13, 2022. [Denish Ochieng, Standard]

The UDA administration begins its work to develop the nation facing significant economic and fiscal challenges. It is an uncanny situation that feels like the one Kenya had 20 years ago when President Mwai Kibaki took over the reins of government from President Daniel Moi.

Subscribe to our newsletter and stay updated on the latest developments and special offers!