×

The Standard e-Paper

Stay Informed, Even Offline

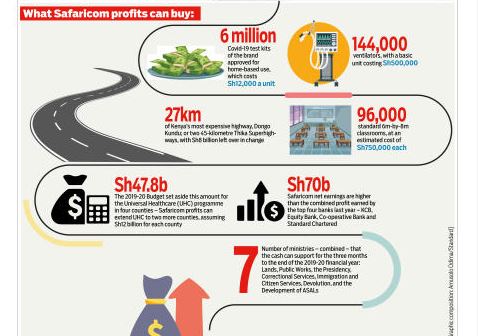

A chart shared online compares the revenue of Safaricom‘s M-Pesa to that of our major banks. Except Equity and KCB, M-Pesa beats the rest hands down.

Subscribe to our newsletter and stay updated on the latest developments and special offers!