The Standard Group Plc is a

multi-media organization with investments in media platforms spanning newspaper

print operations, television, radio broadcasting, digital and online services. The

Standard Group is recognized as a leading multi-media house in Kenya with a key

influence in matters of national and international interest.

For more than ten years after the Cabinet approved the sale of struggling State companies, the Government has suddenly been smitten with an urgency to sell 23 state corporations.

Just days before this revelation, the Privatisation Commission tapped for Chief Executive at Joshua Kulei’s firm - the Sovereign Group Ltd, to spearhead the sale of struggling State firms.

Joseph Kipketer Koskey was the Group chief executive of Sovereign Group, an investment company with diverse interests in various sectors in Kenya and other regions.

“Mr Koskey will be charged with spearheading the Privatisation Commission’s key role of unlocking the potential of State-Owned Enterprises,” the Commission said on email.

Mr Koskey beat 78 other applicants to take over the commission which has been headed by Janerose Omondi on an acting capacity.

While opinion differs on how to go about it, which companies to sell and which ones to retain, analysts view the massive sale as a means for the Government to get quick cash as it struggles with a looming debt crisis.

Adequate preparation of parastatals for privatisation and selling to strategic buyers will generate an overall productivity boost for the economy just like the sale of Kenya Commercial Bank (KCB) shares, Safaricom, Kenya Airways and KenGen, which boosted the capital markets and spurred the State firms’ performance at the time.

“If you look at listed companies where the Government has a substantial shareholding, they make low hanging fruits as scaling down this shareholding could make easier and faster transactions... they can go to market in the shortest time possible,” Derivatives Market Director at the National Securities Exchange (NSE) Terrence Adembesa told a recent forum on privatisation.

However, analysts argue that while privatisation is the way to go, a fire sale shows desperation, will result in undervaluation with the taxpayer getting the short end of the stick.

“Auctioneer mindset to sell the family silver and raise cash quick is not going to be productive in the long term or remunerative in the short term,” Deepak Dave of Riverside Capital said.

Fire-sales

“Privatising companies to raise cash is not always the best motivation. An industrial and economic strategy should underpin the movement of assets from public to private sector; fire-sales never result in the right valuation in cash or value for the economy,” Deepak said.

Sale of State companies has also attracted opposition from heightened interests including County governments, politicians and the current management of some of the corporations.

It’s argued that the bluechip corporations rich enough to sustain its operations are not in need of any kind of help from the private sector. The efficiency of the private sector cannot be questioned, but its involvement in such a profitable organisation will only benefit investors at the cost of solid cash inflows to the exchequer.

Stay informed. Subscribe to our newsletter

Kenya Pipeline Company (KPC) Chairman John Ngumi is resisting the move.

He recently told a parliamentary committee that privatisation might not be the answer to KPC and other State-run entities, with history showing that some entities have been run down after privatisation.

“There are many corporations that have been privatised in the past but they are worse in terms of service delivery. What is important is to make sure that the corporations are properly managed,” Ngumi told the Senate Committee on Energy last week.

The Kenya Dairy Farmers Federation has also opposed the plan to sell the New KCC stating that it has been doing well, stabilising prices and that such critical market intervention would be lacking if the sale goes through.

“I know they have more than 372 acres of land across the country…even in Uganda…the asset value is more than Sh20 billion. We are therefore wondering why they are in hurry to sell this firm?” the chair Mr Richard Tuwei said.

Nakuru Senator Susan Kihika said she will oppose the plan, claiming there could be a plot to sell the firms at throwaway prices to already known individuals. “We suspect these corporations will be under-priced so that they are offloaded cheaply to make money for some people. We shall resist as the Senate,” she said.

It would be like “killing the Goose that laid the golden eggs.” The strong message is that the government should privatize these large companies, if only it identifies operational inefficiencies, to have a better management, technology transfer and transparency. Even then, it could privatize a portion of these public firms only to add value, and not to be sold to a single investor, but to the general public.

Opposition is mounting and possibly a raft of litigation like the counties in the sugar belt have used to stop privatisation of the five sugar mills looms. Some agree that State corporations need to offload shares to increase efficiency, earn the Government taxes and reduce avenues for rewarding political losers.

PKF Chief Executive Atul Shah said the Government needed to fast-track privatising some of its entities as many of them end up performing poorly when left in the hands of the State for too long.

“Staying in Government has left some of the entities in more difficulties... The trends in other markets is that Governments are taking a more aggressive approach in privatising utilities and this is what we need to do,” said Shah.

1.Non-profitable

National Bank and Consolidated Bank

State lenders have often been allowed to test the limits of regulation breaching Central Bank of Kenya’s (CBK) statutory requirements as the Government rescue is usually slow in coming following bureaucratic bottlenecks.

However, the rate at which state lenders repeat the same mistakes that sent them into crisis is a problem of patronising, regulatory soft handedness and an insult to the taxpayer who foot the bill whenever the banks fail.

National Bank of Kenya (NBK) has recently been linked to a sale by the Kenya Commercial Bank (KCB) which would benefit from banking the government and being a State lender secure huge deposits. However KCB has opted to buy Imperial Bank of Kenya - a failed lender that will strain its books thus less likely to turn to NBK.

Meanwhile, NBK has recently been rocked by a scandal of writing off bad loans in the hope that the privatisation will mask the actors once it is sold. But who will be interested in the lender once it loses State goodwill that has often shielded it from the regulator and guaranteed it some form of liquidity through deposits.

Consolidated Bank has come closest to being sold with the Privatisation Commission even seeking a transactional advisor.

It also helps that the current boss Mr Koskey was a director at the bank.

However, Consolidated Bank which needed a Sh500 million boost from Government this year to stay at 20.2 per cent liquidity, just marginally above the 20 per cent required by CBK is not in better shape than it was when nine failing banks were lumped together in 1989 to form it.

The nine insolvent financial institutions that were merged included Jimba Credit Corporation, Union Bank of Kenya Ltd, Kenya Savings and Mortgages Ltd, Estate Finance Company of Kenya Ltd, Estate Building Society, Business Finance Company, Citizen Building Society, Nationwide Finance Company and Home Savings and Mortgages Ltd. Now it is a loss-making accumulation of its historic past.

Uchumi

Uchumi is also a case of State companies that have persistently cost the tax payers money to be saved but still ended up failing. It is one of the listed firms that has missed the deadline to publish results as set by the Capital Markets Authority (CMA).

After being rescued by President Mwai Kibaki when it died in 2006 with a State sponsored deal that saw KCB and PTA Bank come to the rescue of Uchumi Supermarket by converting their debts into shares.

Last year, attempts to save the premier supermarket saw it burn through the Sh700 million State bailout in just months.

It is back in court to defend its life and selling it off will be better for the state rather than throwing good money after bad money.

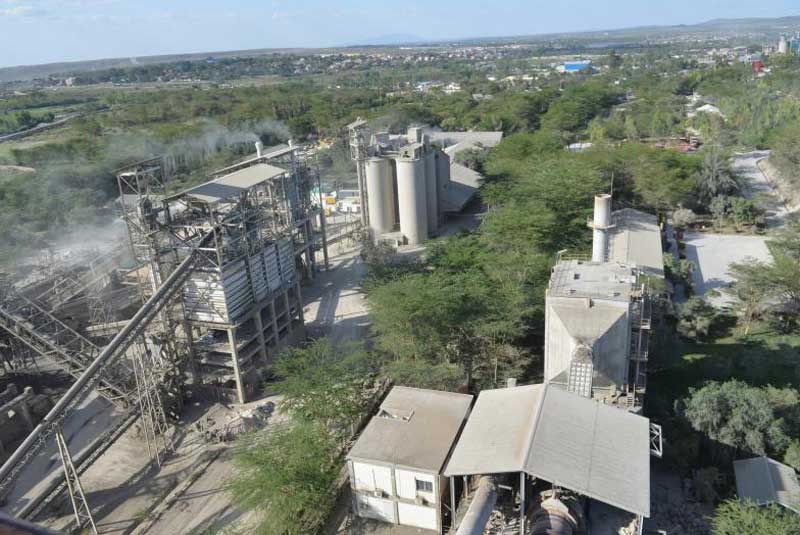

Portland Cement

East African Portland Cement is operating at half capacity, it is overstaffed, with some of its production lines remaining idle. Its market share is dwindling yet it owes creditors Sh10.9 billion and a further Sh2 billion to revamp its plant plus additional money for buying stocks and for working capital.

It could grind taxpayer’s money unless it sells its land even as local politicians and surrounding communities who have laid claim to the land protest.

Presiding chair and representative of LafargeHolcim Kungu Gatabaki said that locals were sceptical that a privatisation bid would see them lose out.

He was optimistic that the Government will consider selling a stake to them as well as county government to get value from the firm once it picks off from State bureaucracy.

The Five sugar millersCane hauling tractors block Miwani-Kibos road in Kisumu County. Most millers in the sugar belt face financial woes. [File, Standard]

Everyone has been in agreement that the government running sugar mills in the Western belt has spurred inefficiency, saddled the companies with over Sh50 billion debt burden and kept the price of local sugar up in a protectionist policy that has restricted the entry of the product from the Common Market for Eastern and Southern Africa (Comesa).

The Government tried to sell 51 per cent stake in the five millers to strategic investors, while another 24 per cent was set aside for farmers and employees.

However, Governors and politicians from the sugar belt in Western Kenya have blocked plans to privatise Chemelil Sugar Company, South Nyanza Sugar Company, Nzoia Sugar Company, Miwani Sugar Company (in receivership) and Muhoroni Sugar Company (in receivership), saying the Privatisation Commission has failed to comply with the law. Mumias has also failed to release the results on time as stipulated by the CMA.

At the centre of the dispute is the 41,411.47 acres of land, equivalent to 31,372 football fields, where the companies own extensive tracts that may be ripe for grabbing. Chemelil has 6,868 acres, Nzoia 11,438 acres, South Nyanza 7,407 acres while Muhorini has 6,866 acres. Miwani has 8,831 acres.

The State will have to balance these interest if it is to successfully navigate their privatisation even as the end of the safeguards against the 19-member Comesa countries beckon.

2.Profitable firms

But on the flip side, the state is running some very lucrative firms that would ideally earn the exchequer significant income if the privatization is done above board in a deliberate way to benefit the Nairobi Securities Exchange Market and spur efficiency even further.

Mr Shah, the PKF executive said that the Privatisation Commission needed to examine the financial status of the different firms that are up for sale and classify them depending on their health.

“If we categorise the companies so that, for instance, we have an ‘A’ list for companies that are ready for sale and a ‘C’ list for companies that will need a little more work before they can be privatised, we will do more justice to them,” he said.

Kenya Pipeline Company

With an asset base of Sh93 billion and reporting a profit after tax of Sh8.4 billion, according to its annual report for 2016, the pipeline company easily passes for a blue chip company. So liquid is the firm that when it embarked on building the Sh1.7 billion jetty on Lake Victoria, it financed it internally.

KPC’s earnings are tipped to grow considering the projects that it has recently engaged in including the new Mombasa-Nairobi pipeline that is expected to take to a substantial chunk of business from truckers.

This is due to cost-effectiveness as well as the Kisumu Jetty that is expected to grow marine transportation of petroleum to neighbouring countries especially to Uganda and Northern Tanzania.

It also has an elaborate growth plan for the next decade that is expected to see it have operations in the neighbouring countries.

The healthy profits and balance sheet by the company as well as the generally attractive nature of the petroleum business and its opaqueness in the country have seen KPC attract its fair share of rogue elements.

It is currently the subject of several probes by the Ethics and Anti-Corruption Commission (EACC) that is looking into alleged incidences where KPC may have lost money in fraudulent deals.

KPC last week fought the planned privatisation. John Ngumi chairman KPC board told Senate’s Department Committee on Energy that the decision to sell state-owned companies as ‘irrational and illogical’ and that the Government should instead ensure proper running of the firms instead of selling them.

Kenya Ports Authority (KPA)

The agency may have blundered big time over the last few months and ended with more cargo at its Inland Container Depot (ICD) in Nairobi than it knew what to do with it.

The debacle that led to congestion at the ICD is a pointer to the inefficiencies that have for years dogged KPA and some importers, especially from neighbouring countries, give serious thought to alternatives such as Dar es Salaam.

While such an alternative is viable for some importers, for instance from Rwanda, the Mombasa Port remains a key option for Kenya, Uganda and even South Sudan.

Kenya is still a preferred import route for some businesses in Rwanda and even further to Eastern DRC.

And it is partly because of the captive nature of its clients that KPA has remained in business despite inefficiencies and other ills that have afflicted the authority.

Thus, it has through the years remained a performer in terms of earnings and consistently returned a divided to the National Treasury. Privatisation could hand over key hubs such as the Port in Mombasa as well as those planned in Lamu to private hands.

The ports authority reported a net profit of Sh6.6 billion in the year to June 2016. Revenues stood at Sh38 billion while total assets were at Sh150 billion.

New KCC

The milk processor reported a Sh39.77 million profit in the year to June 2016, which is the most recent annual report available.

This is an improved position when compared to a loss of Sh66.86 the previous year. While it has struggled to keep up with the privately owned milk firms bogged down by bureaucracies associated with Government ownership, New KCC has put on a fairly bold fight and commands a significant share of the processed milk market.

Despite having to contend with Government processes, New KCC commands a 35 per cent market share in the fast-paced industry as of December 2017. This is in comparison to a 40 per cent share by Brookside Dairy, whose ownership is linked to the Kenyatta family and which has over the recent past acquired rivals such as Buzeki Dairy, Delamere and SpinKnit.

Githunguri Dairy Farmers Cooperative, which owns the Fresha brand has a share of 10 per cent.

Privatisation would leave the processed milk industry in the hands of private players and whose casualties will be the farmers and consumers.

While New KCC has had to sustain itself with little help from the Government, the State ownership has ensured that it plays a critical role in the stabilisation of milk prices for both the farmer and the consumer.

Intercontinental, Hilton and Mountain LodgeHilton hotel. [File, Standard]

There are more than eight hotels where Government shareholding is up for sale. Only three, however, are sound enough to attract investors and have received all the approvals.

Intercontinental, where the Government through the Tourism Finance Corporation has a 40 per cent stake, Hilton Hotel (33.83 per cent) and Mountain Lodge (39.11 per cent) were to be sold off but the Privatisation Commission put the process on hold as the bid it received did not match the value of the hotels.

It attributed the low offers to turbulent times that the tourism industry was experiencing in 2014 and 2015.

The Commission said the bullish sentiment in the industry was likely to bring back investors on the table with much better offers but does not have a time line for taking the hotels back to the market. Other investors that have stakes in the in hotels have pre-emptive rights.

The three hotels are major players in the country’s tourism sector and while they may have taken a beating in the recent years following a slump in the industry earnings, it is now on the rise with optimism that it will sustain growth in the coming years.

Other hotels where the Government plans to offload shareholding are Kabarnet Hotel, where the Government owns 98.2 per cent, Mt Elgon Lodge (72.92 per cent), Kakamega Golf (80 Per cent), Sunset Hotel (95.4 per cent) and Kenya Safari Lodges and Hotels (63.42 per cent – which runs the Mombasa Beach Hotel, Voi Safari Lodge and Ngulia Safari Lodge).

Kenya Wine Agencies Ltd (Kwal)

The Government plans to sell its stake in the alcoholic beverage manufacturer and is yet to decide whether to sell to a strategic investor or offload to the public through an Initial Public Offer. It currently owns 42.65 per cent in Kwal through the Industrial and Commercial Development Corporation (ICDC).

It had set aside a four per cent stake to sell to employees who took up an insignificant proportion, with the balance going back to ICDC. South Africa’s Distell owns a majority 52.43 per cent after it acquired a 26 per cent shareholding from Centum.

The firm makes alcoholic brands such as Kibao Vodka while exclusively importing and distributing Distell’s brands such as Amarula and Viceroy Brandy in Kenya.

As with other players in the industry, the firm expects growth with consumption of alcoholic drinks expected to continue on an upward trajectory.

The Standard Group Plc is a

multi-media organization with investments in media platforms spanning newspaper

print operations, television, radio broadcasting, digital and online services. The

Standard Group is recognized as a leading multi-media house in Kenya with a key

influence in matters of national and international interest.

The Standard Group Plc is a

multi-media organization with investments in media platforms spanning newspaper

print operations, television, radio broadcasting, digital and online services. The

Standard Group is recognized as a leading multi-media house in Kenya with a key

influence in matters of national and international interest.